Is the Real Estate Housing Market Crashing?

Is the real estate housing market crashing? It’s a question on everyone’s mind as interest rates rise, inflation soars, and economic uncertainty looms. The recent surge in home prices, fueled by low interest rates and a pandemic-driven housing boom, has left many wondering if a correction is on the horizon.

While the current market is showing signs of cooling, predicting a crash is a complex endeavor that requires a deep dive into multiple factors.

This article will explore the current market trends, economic factors, key indicators, and buyer and seller behavior to shed light on the potential for a housing market crash. We’ll analyze the historical patterns of housing market cycles and discuss the long-term outlook for the industry, providing a balanced perspective on the risks and opportunities ahead.

Current Market Trends

The real estate market is a dynamic entity, constantly influenced by a multitude of factors. Understanding current trends is crucial for anyone involved in buying, selling, or investing in properties. Let’s delve into the recent shifts in home prices, sales volume, interest rates, and other key indicators that shape the current market landscape.

Home Prices and Sales Volume

Recent changes in home prices and sales volume across major regions provide valuable insights into the market’s direction. While prices have been rising steadily for several years, recent data suggests a shift in this trend. In some areas, home prices have begun to stabilize or even decline slightly, indicating a potential cooling of the market.

Sales volume, a measure of the number of homes sold, has also slowed down in several regions. This decrease in sales volume can be attributed to a combination of factors, including rising interest rates, affordability concerns, and a growing inventory of homes for sale.

Interest Rates and Affordability

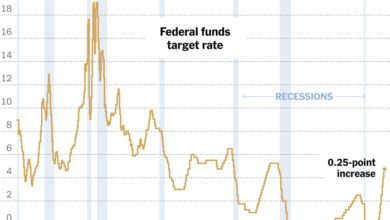

Interest rates play a significant role in determining home affordability. As interest rates rise, the cost of borrowing money for a mortgage increases, making homeownership less accessible for many buyers. Comparing current interest rates with historical data reveals a significant increase in recent months.

This rise in interest rates has directly impacted affordability, pushing some potential buyers out of the market.

For example, a 30-year fixed-rate mortgage with a 5% interest rate will result in a higher monthly payment compared to a 3% interest rate, all other factors being equal.

Key Factors Driving Market Conditions

The current market conditions are influenced by a complex interplay of economic indicators, inflation, and consumer sentiment.

- Economic Indicators:Economic growth, employment levels, and consumer confidence all contribute to the overall health of the real estate market. When the economy is strong, people tend to have more disposable income, which can lead to increased demand for housing. Conversely, economic downturns can result in reduced demand and slower price growth.

- Inflation:Rising inflation erodes purchasing power and can make it more challenging for people to afford a home. As prices for goods and services increase, consumers have less money left over for housing expenses.

- Consumer Sentiment:Consumer sentiment, which reflects how optimistic or pessimistic people are about the economy, can significantly impact housing demand. When consumers are confident about the economy, they are more likely to make major purchases, including homes.

Inventory Levels and Supply and Demand Dynamics

Inventory levels, which refer to the number of homes available for sale, play a crucial role in shaping supply and demand dynamics. In a seller’s market, inventory levels are typically low, giving sellers more leverage in negotiations. Conversely, a buyer’s market is characterized by higher inventory levels, giving buyers more options and negotiating power.

For example, if there are fewer homes available for sale than buyers looking to purchase, sellers are in a stronger position to command higher prices.

Economic Factors

The housing market is intricately linked to the overall health of the economy. Economic fluctuations, such as recessions, inflation, and interest rate changes, can significantly impact housing prices, affordability, and demand.

Recessionary Fears and Economic Uncertainty

Recessions are periods of economic decline characterized by falling GDP, rising unemployment, and reduced consumer spending. During a recession, job losses and reduced income can lead to a decline in housing demand, as people become more cautious about making large financial commitments.

Moreover, economic uncertainty can make lenders more hesitant to approve mortgages, further dampening market activity. For example, the 2008 financial crisis, triggered by the housing market crash, resulted in a significant economic recession, with widespread job losses and a sharp decline in housing prices.

Inflation, Rising Interest Rates, and Housing Affordability

Inflation is a sustained increase in the general price level of goods and services. Rising inflation erodes purchasing power, making it more expensive for consumers to buy homes. Furthermore, central banks often raise interest rates to combat inflation, which increases the cost of borrowing money, making mortgages more expensive.

This combination of inflation and higher interest rates can significantly impact housing affordability, making it challenging for potential homebuyers to qualify for mortgages or afford monthly payments. For instance, in 2022, the Federal Reserve aggressively raised interest rates to combat rising inflation, resulting in a significant increase in mortgage rates and a slowdown in housing demand.

Government Policies and Housing Market

Government policies play a crucial role in shaping the housing market. Tax incentives, such as deductions for mortgage interest and property taxes, can encourage homeownership and stimulate demand. Conversely, regulations, such as zoning laws and building codes, can influence housing supply and affordability.

It’s hard to say for sure if the real estate housing market is crashing, but it’s definitely a hot topic. There are a lot of factors at play, including rising interest rates and inflation. It’s interesting to note that even the skies are being monitored for their impact on climate change, as airlines must monitor vapour trails under new EU climate rules.

While this might seem unrelated, it shows how the world is becoming more aware of environmental impacts, which could potentially affect the housing market as well. Only time will tell what the future holds for the real estate market.

For example, the Tax Cuts and Jobs Act of 2017 temporarily increased the standard deduction for homeowners, potentially boosting homeownership rates. Additionally, government-sponsored enterprises (GSEs), such as Fannie Mae and Freddie Mac, play a significant role in the mortgage market by providing liquidity and stability.

Global Economic Events and the US Housing Market

The US housing market is not immune to global economic events. Trade wars, global recessions, and geopolitical tensions can impact the economy and, consequently, the housing market. For example, the COVID-19 pandemic led to global supply chain disruptions and economic uncertainty, which affected the housing market.

Similarly, the ongoing war in Ukraine has created economic instability and volatility, impacting global markets and potentially influencing the US housing market.

Market Indicators

Understanding the key housing market indicators can provide valuable insights into the current state of the market and help predict future trends. These indicators reflect the overall health of the housing market and offer a comprehensive view of supply, demand, and pricing dynamics.

Key Housing Market Indicators

Several key housing market indicators provide valuable insights into the health and direction of the real estate market.

- Case-Shiller Home Price Index (CS HPI):This index tracks changes in home prices in 20 major metropolitan areas across the United States. It is a widely recognized indicator of home price appreciation and is often used to assess the overall health of the housing market.

The real estate market is a rollercoaster, with ups and downs that can leave us all feeling a bit uncertain. It’s hard to ignore the news headlines about potential crashes, but sometimes it’s important to remember the human stories behind these economic shifts.

Just this week, the world was saddened by the tragic news of the passing of Michaela Mabinty Deprince’s mother, Elaine, within 24 hours of each other. This heartbreaking story reminds us that even amidst economic fluctuations, life goes on, and we must continue to find ways to connect and support each other.

Whether the housing market is crashing or soaring, it’s the human stories that ultimately matter most.

The CS HPI is a leading indicator, meaning it can signal future trends in the housing market.

- Pending Home Sales Index (PHSI):The PHSI measures the number of homes that have gone under contract, providing a glimpse into future home sales. This index is a leading indicator of future home sales activity, as it reflects the level of buyer demand and the pace of transactions.

A rising PHSI suggests increased buyer activity and potential for future price growth.

- Existing Home Sales (EHS):This indicator measures the number of existing homes that are sold each month. It provides insights into the overall level of housing market activity and is a lagging indicator, reflecting past trends in the market. A decline in EHS could indicate a slowdown in demand or a weakening housing market.

- New Home Sales (NHS):This indicator measures the number of newly constructed homes that are sold each month. It reflects the level of construction activity and the demand for new homes. A rise in NHS suggests increased demand and potential for future price growth in the new home market.

- Inventory of Homes for Sale:This indicator tracks the number of homes available for sale in the market. A low inventory level suggests a seller’s market, where demand outpaces supply, leading to potential price increases. Conversely, a high inventory level suggests a buyer’s market, where supply exceeds demand, potentially leading to price declines.

The question of whether the real estate housing market is crashing is on everyone’s mind, and it’s a topic that’s likely to be a major talking point in the upcoming elections. While the economy is a major factor, the recent rally for union support by Kamala Harris and Tim Walz in crucial blue wall states, as reported in this article , could have a significant impact on the housing market.

Unions are often a strong voice for affordable housing and worker rights, which can influence policy decisions that impact housing affordability and availability. Ultimately, the future of the real estate market is intertwined with these political and economic factors.

Performance of Key Indicators Over the Past Year

The performance of key housing market indicators over the past year has been mixed, reflecting the complex dynamics of the market. The Case-Shiller Home Price Index, for instance, has shown a slowdown in price growth, indicating a potential shift from the rapid appreciation seen in previous years.

The Pending Home Sales Index has also experienced fluctuations, reflecting the impact of rising mortgage rates and economic uncertainty on buyer sentiment.

Relationship Between Market Indicators and Consumer Confidence

Consumer confidence plays a significant role in the housing market, influencing buyer and seller behavior. When consumer confidence is high, individuals are more likely to purchase homes, leading to increased demand and potentially higher prices. Conversely, low consumer confidence can lead to decreased demand and potential price declines.

Market indicators, such as the Case-Shiller Home Price Index and the Pending Home Sales Index, can provide insights into consumer confidence levels. For example, a decline in the Case-Shiller Home Price Index may signal weakening consumer confidence and a potential slowdown in the housing market.

Current Values and Historical Trends of Key Housing Market Indicators

| Indicator | Current Value | Year-Over-Year Change | Historical Trend (Past 5 Years) |

|---|---|---|---|

| Case-Shiller Home Price Index | [Insert Current Value] | [Insert Year-Over-Year Change] | [Insert Historical Trend] |

| Pending Home Sales Index | [Insert Current Value] | [Insert Year-Over-Year Change] | [Insert Historical Trend] |

| Existing Home Sales | [Insert Current Value] | [Insert Year-Over-Year Change] | [Insert Historical Trend] |

| New Home Sales | [Insert Current Value] | [Insert Year-Over-Year Change] | [Insert Historical Trend] |

| Inventory of Homes for Sale | [Insert Current Value] | [Insert Year-Over-Year Change] | [Insert Historical Trend] |

Buyer and Seller Behavior

The current real estate market is characterized by a shift in buyer and seller behavior, influenced by economic factors, interest rates, and market expectations. Understanding these dynamics is crucial for navigating the market effectively.

Comparison with Historical Trends

The current buying and selling activity is significantly different from historical trends. Historically, periods of high demand and low inventory often resulted in rapid price appreciation. However, the current market is experiencing a slowdown in both buying and selling activity.

This is due to several factors, including:

- Higher interest rates:Rising interest rates have made mortgages more expensive, reducing affordability for many buyers.

- Inflation:High inflation has eroded purchasing power, leading to a decrease in demand for housing.

- Economic uncertainty:Concerns about a potential recession have made some buyers hesitant to commit to large purchases.

Motivations of Buyers and Sellers

The motivations of buyers and sellers in the current market are shaped by the prevailing economic conditions.

- Buyers:Many buyers are motivated by a desire to find a home at a more affordable price, especially as interest rates have risen. Some buyers are also seeking larger homes or more space due to the shift to remote work and the need for home offices.

- Sellers:Sellers are facing a more challenging market, with slower sales and potential for lower prices. Some sellers are motivated to sell due to job relocation, downsizing, or financial reasons. Others may be hesitant to sell, waiting for the market to rebound.

Impact of Affordability Challenges on Buyer Behavior

Affordability challenges are significantly impacting buyer behavior.

- Reduced buying power:Higher interest rates and inflation have reduced the buying power of many potential homebuyers. This has resulted in a decline in demand for homes, especially in higher-priced markets.

- Increased competition for lower-priced homes:As buyers seek more affordable options, competition for lower-priced homes has intensified. This can lead to bidding wars and multiple offers, making it difficult for buyers to secure a property.

- Shifting preferences:Some buyers are adjusting their preferences to accommodate affordability challenges. This may include seeking smaller homes, exploring different neighborhoods, or delaying homeownership.

Factors Influencing Seller Decisions

Seller decisions are influenced by a combination of factors, including:

- Market expectations:Sellers are closely watching market trends and economic indicators to gauge future price movements. Some sellers may be hesitant to sell if they expect prices to rebound in the future.

- Inventory levels:High inventory levels can create a competitive selling environment, potentially leading to lower selling prices. Sellers may be more inclined to sell if inventory is low and demand is high.

- Personal circumstances:Personal circumstances, such as job relocation, family changes, or financial needs, can also influence a seller’s decision to list their property.

Long-Term Outlook: Is The Real Estate Housing Market Crashing

Predicting the future of the housing market is inherently challenging, as it’s influenced by a complex interplay of economic, social, and technological factors. However, understanding historical trends, current market dynamics, and potential future shifts can help us gain insights into the long-term outlook.

Potential for a Housing Market Crash

While a housing market crash is always a possibility, its likelihood and severity depend on a confluence of factors.

- Rising Interest Rates:Higher interest rates make mortgages more expensive, reducing affordability and potentially slowing down demand.

- Inflation:Persistent inflation can erode purchasing power and lead to a decline in housing demand, especially if wages don’t keep pace.

- Economic Recession:A significant economic downturn can lead to job losses and reduced consumer confidence, negatively impacting housing demand.

- Overvaluation:If home prices rise significantly faster than underlying economic fundamentals, a correction could occur to bring prices back in line with market realities.

- Overbuilding:A surplus of new homes can create a glut in the market, putting downward pressure on prices.

Historical Patterns of Housing Market Cycles

Housing markets typically exhibit cyclical patterns, characterized by periods of growth and decline.

- Boom-Bust Cycles:Historically, housing markets have experienced boom periods with rapid price appreciation followed by busts with sharp price declines. These cycles can last for several years.

- Average Cycle Duration:The duration of housing cycles varies, but they typically range from 5 to 10 years. However, recent cycles have been shorter and more volatile due to factors like deregulation and financial innovation.

- Historical Examples:The housing bubble of the early 2000s, which led to the financial crisis of 2008, is a prime example of a housing market crash. Other examples include the housing busts of the 1980s and 1990s.

Impact of Demographic Shifts and Technological Advancements, Is the real estate housing market crashing

Demographic shifts and technological advancements are likely to have a significant impact on the long-term outlook for housing.

- Aging Population:As the population ages, demand for single-family homes may decline, while demand for senior housing and assisted living facilities may increase.

- Urbanization:Continued urbanization and population growth in major cities could lead to increased demand for housing in these areas, potentially driving up prices.

- Remote Work:The rise of remote work has the potential to reshape housing preferences, with people seeking larger homes in more affordable locations outside major cities.

- Technological Advancements:Advancements in construction technologies, such as modular homes and 3D printing, could lead to increased affordability and faster construction times.

Risks and Opportunities in the Housing Market

The housing market presents both risks and opportunities for investors and homeowners.

- Risks:As mentioned earlier, potential risks include rising interest rates, economic recession, and overvaluation. It’s crucial to consider these factors when making investment decisions.

- Opportunities:Long-term growth in the housing market is driven by fundamental factors like population growth and urbanization. Opportunities exist for those who can identify undervalued properties and capitalize on long-term trends.