Blockchain Basics and Its Role in Bitcoin

Blockchain basics and its role in Bitcoin are fundamental to understanding the future of finance and technology. Imagine a digital ledger, shared across a network of computers, where every transaction is permanently recorded and accessible to everyone. This is the essence of blockchain, a revolutionary technology that underpins Bitcoin and is transforming various industries.

Bitcoin, the first and most well-known cryptocurrency, relies on blockchain to ensure secure and transparent transactions. Every Bitcoin transaction is recorded on a blockchain, creating a permanent, auditable record. This eliminates the need for intermediaries like banks, empowering individuals to control their finances directly.

Introduction to Blockchain

Imagine a digital ledger that’s shared and synchronized across a network of computers, making it virtually impossible to alter or tamper with. That’s the essence of blockchain technology. It’s a revolutionary concept that’s reshaping industries, from finance to healthcare.Blockchain is a decentralized, distributed ledger that records transactions in a secure and transparent manner.

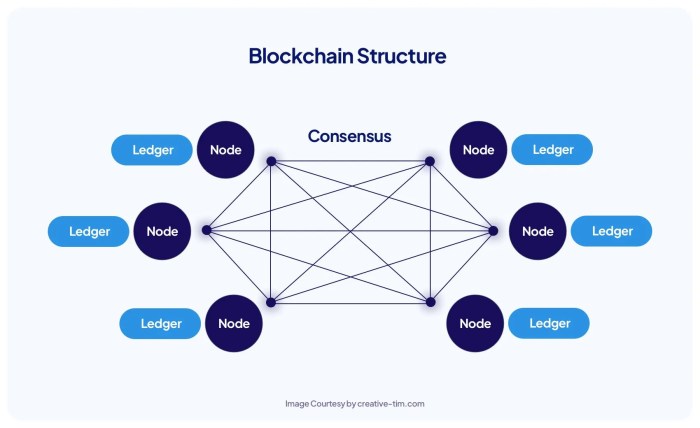

Unlike traditional databases, which are centralized and controlled by a single entity, blockchain is distributed across multiple computers, eliminating the need for a central authority.

Blockchain’s Decentralized Nature

Blockchain’s decentralized nature is its defining characteristic. It ensures that no single entity has complete control over the data, making it highly resistant to manipulation and censorship.

Understanding blockchain basics is crucial for grasping the mechanics of Bitcoin. It’s essentially a distributed ledger, recording every transaction transparently and immutably. This technology, underpinning Bitcoin, is also being explored for other applications, like securing sensitive information. For instance, the recent news that a Trump lawyer told the Justice Department that classified material had been returned raises questions about data security and accountability, highlighting the potential of blockchain to enhance these aspects in various domains.

- Each block in the blockchain contains a record of transactions, and each block is linked to the previous one, forming a chain. This chain of blocks is distributed across a network of computers, called nodes.

- To modify a transaction in the blockchain, a hacker would need to alter the data in every single block, which is practically impossible due to the decentralized nature of the network.

Blockchain as a Distributed Ledger

A distributed ledger is a shared database that’s replicated across multiple computers. This ensures that all participants have access to the same information, promoting transparency and trust.

- Unlike traditional databases, which are centralized and controlled by a single entity, blockchain is distributed across multiple computers, making it resistant to single points of failure and manipulation.

- Every transaction is recorded in the blockchain, creating a permanent and immutable record of events. This transparency and immutability make blockchain a powerful tool for tracking and verifying data.

History of Blockchain

The concept of blockchain emerged in 1991 with the invention of the “hashcash” proof-of-work system by Stuart Haber and W. Scott Stornetta. Their goal was to create a system for time-stamping documents, preventing them from being tampered with.

Blockchain technology, the backbone of Bitcoin, ensures secure and transparent transactions by creating a permanent record of every exchange. This immutable ledger, with its decentralized nature, is a stark contrast to the murky world of classified documents, where the very definition of “declassified” can be debated endlessly.

The recent controversy surrounding Trump’s claims of declassifying documents at Mar-a-Lago highlights the importance of clear, verifiable records, a principle that blockchain champions. While Bitcoin may be a digital currency, its underlying technology provides a powerful lesson in the importance of transparency and accountability, even in the face of complex legal and political disputes.

- In 2008, Satoshi Nakamoto, a pseudonym believed to be a group of individuals, published a white paper outlining a decentralized digital currency called Bitcoin. This paper introduced the concept of a blockchain to secure and manage Bitcoin transactions.

- Since then, blockchain technology has evolved rapidly, with various applications beyond cryptocurrency. Today, blockchain is being explored in various industries, including finance, healthcare, supply chain management, and more.

Key Features of Blockchain

The blockchain is a revolutionary technology that underpins cryptocurrencies like Bitcoin. It is a distributed ledger that records transactions in a secure and transparent manner. Let’s delve into the key features that make blockchain so unique and powerful.

Immutability

Immutability is a core principle of blockchain, meaning that once a transaction is recorded on the blockchain, it cannot be altered or deleted. Each block in the chain is cryptographically linked to the previous block, creating an unbroken chain of records.

This immutability ensures the integrity and reliability of the data stored on the blockchain.

Transparency

Transparency is another key feature of blockchain. All transactions on the blockchain are publicly visible and can be accessed by anyone. This transparency fosters trust and accountability, as all participants can verify the validity of transactions.

Consensus Mechanisms

Blockchain relies on consensus mechanisms to ensure that all participants agree on the state of the ledger. These mechanisms involve a process where nodes in the network validate and confirm transactions. A common consensus mechanism is Proof-of-Work (PoW), where miners compete to solve complex mathematical problems to add new blocks to the chain.

Understanding blockchain basics is essential for grasping how Bitcoin operates, and it’s a concept that can be applied to various real-world scenarios. Just like Bitcoin’s decentralized ledger ensures secure and transparent transactions, a robust infrastructure is vital for ensuring essential services, such as water supply.

Take, for example, the recent water crisis in Jackson, Mississippi, how Jackson Mississippi ran out of water highlighting the need for reliable systems and infrastructure. Similarly, blockchain’s inherent transparency and immutability can contribute to better management and accountability in vital resources, offering a glimpse into the potential for future applications beyond just cryptocurrency.

The first miner to solve the problem receives a reward in the form of cryptocurrency.

Role of Cryptography, Blockchain basics and its role in bitcoin

Cryptography plays a vital role in securing blockchain transactions. Each transaction is encrypted using cryptographic algorithms, making it extremely difficult to tamper with or forge. Public-key cryptography is used to generate unique addresses for each user, ensuring anonymity and privacy.

Types of Blockchains

Blockchains can be classified into different types based on their access and governance models. Here are some common types:

- Public Blockchains: Public blockchains are open to anyone and allow anyone to participate in the network. Bitcoin and Ethereum are examples of public blockchains.

- Private Blockchains: Private blockchains are controlled by a single entity or organization. Access and permissions are restricted, and transactions are not publicly visible.

- Consortium Blockchains: Consortium blockchains are a hybrid model where multiple organizations collaborate to govern the network. Access is restricted to authorized members, but the network is more decentralized than a private blockchain.

Blockchain and Bitcoin

Bitcoin is the most well-known and widely used cryptocurrency, and it is built upon the foundation of blockchain technology. This relationship is fundamental, as blockchain acts as the backbone for Bitcoin’s operations.

Bitcoin Transactions and the Blockchain

Bitcoin transactions are recorded and verified on the blockchain, which serves as a distributed ledger, a public record of every transaction that has ever occurred on the Bitcoin network. Each transaction is grouped together into a block, and these blocks are chained together chronologically, forming the blockchain.

Each block contains a hash of the previous block, creating a chain of blocks that are linked together. This structure ensures that the blockchain is tamper-proof, as any alteration to a block would invalidate the hashes of all subsequent blocks.

To illustrate this, imagine a chain of paper clips. Each paper clip represents a block, and they are connected to each other. If you try to change the order of the paper clips or remove one, the entire chain will be disrupted.

When a Bitcoin transaction is initiated, it is broadcast to the network and included in a block. Miners, who are individuals or groups that verify and add blocks to the blockchain, process these transactions. The process of verifying and adding blocks is known as mining.

The Role of Miners in Bitcoin

Miners play a crucial role in securing the Bitcoin network and processing transactions. They use powerful computers to solve complex mathematical problems, which is a process called mining. The first miner to solve a problem adds the next block to the blockchain, and they are rewarded with Bitcoin.

This process, known as Proof-of-Work (PoW), ensures that the blockchain remains secure and prevents malicious actors from manipulating the network. Miners also contribute to the network by verifying transactions and preventing double-spending. Double-spending occurs when a user tries to spend the same Bitcoin twice.

Miners ensure that this does not happen by verifying that each Bitcoin is only spent once. The process of mining is competitive, as miners race to solve the mathematical problems first. This competition helps to maintain the security of the network, as it would be very difficult for a single entity to control a majority of the network’s computing power.

Applications of Blockchain Beyond Bitcoin: Blockchain Basics And Its Role In Bitcoin

While blockchain technology is most famously associated with cryptocurrencies like Bitcoin, its potential applications extend far beyond digital money. Blockchain’s inherent features, such as transparency, security, and immutability, make it a powerful tool for revolutionizing various industries and processes.

Supply Chain Management

Blockchain can enhance supply chain management by providing a secure and transparent record of goods’ origin, movement, and ownership.

- Increased Transparency:Blockchain’s decentralized and immutable ledger allows all participants in a supply chain to access the same information, fostering trust and accountability. For example, consumers can track the origin of their food products, ensuring ethical sourcing and sustainability.

- Improved Traceability:By recording every transaction and movement of goods on the blockchain, businesses can quickly identify and trace products in case of recalls or counterfeiting. This helps reduce risks and maintain consumer confidence.

- Enhanced Efficiency:Blockchain streamlines supply chain processes by automating tasks like order tracking and inventory management. This reduces manual errors, saves time, and improves overall efficiency.

For instance, Walmart uses blockchain to track the origin of its leafy greens, ensuring food safety and preventing outbreaks. Similarly, pharmaceutical companies are implementing blockchain to combat counterfeit drugs and guarantee the authenticity of their products.

Healthcare

Blockchain can revolutionize healthcare by improving data security, patient privacy, and interoperability.

- Secure and Private Data Storage:Blockchain’s encrypted and decentralized nature ensures that patient medical records are stored securely and can only be accessed with the patient’s consent. This addresses concerns about data breaches and unauthorized access.

- Efficient Data Sharing:Blockchain facilitates secure and efficient data sharing between healthcare providers, enabling seamless patient care and reducing administrative burden.

- Enhanced Interoperability:Blockchain can help create a unified healthcare system by enabling interoperability between different electronic health record systems, allowing for better coordination of care.

For example, the Medicalchain platform uses blockchain to securely store and share patient medical records, empowering individuals to control their health data. Additionally, companies like Chronicled are developing blockchain solutions to track the movement of pharmaceutical drugs, ensuring their authenticity and preventing counterfeit medications.

Voting Systems

Blockchain can enhance voting systems by increasing transparency, security, and trust.

- Secure and Tamper-Proof Voting:Blockchain’s immutability ensures that votes are recorded accurately and cannot be altered or tampered with. This eliminates the risk of fraud and ensures the integrity of the election process.

- Increased Transparency:All voting records are publicly accessible on the blockchain, allowing for greater transparency and accountability in the electoral process.

- Reduced Costs:Blockchain-based voting systems can potentially reduce the costs associated with traditional voting methods, such as paper ballots and manual counting.

Several countries and organizations are exploring blockchain-based voting solutions. For instance, the Estonian government uses blockchain to secure its national elections, while the Swiss canton of Zug has experimented with blockchain-based voting in local elections.

Challenges and Future of Blockchain

While blockchain technology holds immense potential, it faces several challenges that need to be addressed for widespread adoption. These challenges include scalability, regulatory concerns, and energy consumption. Despite these hurdles, ongoing research and development efforts are paving the way for a future where blockchain transforms various industries.

Scalability

Scalability refers to the ability of a blockchain network to handle increasing transaction volumes without compromising performance. Current blockchains, such as Bitcoin, can only process a limited number of transactions per second, leading to delays and higher transaction fees during peak periods.

- Transaction throughput:The number of transactions a blockchain can process per second is a key indicator of its scalability. Existing blockchains like Bitcoin have a limited transaction throughput, making them unsuitable for high-volume applications.

- Transaction latency:The time it takes for a transaction to be confirmed and added to the blockchain is another crucial aspect. High latency can hinder real-time applications and user experience.

- Scalability solutions:Researchers and developers are exploring various solutions to address scalability challenges, including:

- Sharding:Dividing the blockchain into smaller fragments called shards, allowing parallel processing of transactions.

- Layer-2 scaling solutions:Building separate networks on top of the base blockchain to handle transactions off-chain, reducing congestion on the main chain.

- Off-chain computation:Performing computations and data storage outside the blockchain, only recording the results on the chain to improve efficiency.

Regulatory Concerns

The decentralized and transparent nature of blockchain technology poses challenges for regulators, who are accustomed to traditional financial systems with centralized control.

- Anti-money laundering (AML) and know-your-customer (KYC) regulations:Traditional financial institutions are subject to strict AML and KYC regulations to prevent money laundering and other illicit activities. Implementing these regulations on decentralized blockchain networks presents unique challenges.

- Data privacy and security:Blockchain networks are designed to be transparent, with all transactions recorded on a public ledger. This transparency raises concerns about data privacy and security, especially for sensitive information.

- Taxation and legal frameworks:The lack of clear legal frameworks and tax regulations for blockchain assets creates uncertainty for both users and businesses.

Energy Consumption

Proof-of-work (PoW) consensus mechanisms, used by blockchains like Bitcoin, require significant computational power to validate transactions and secure the network. This energy-intensive process has drawn criticism for its environmental impact.

- Environmental impact:The energy consumption of PoW blockchains is a major concern, particularly in light of climate change.

- Alternative consensus mechanisms:Researchers are exploring alternative consensus mechanisms that are more energy-efficient, such as proof-of-stake (PoS). PoS relies on the amount of cryptocurrency held by validators, rather than computational power, to secure the network.

- Energy efficiency initiatives:Efforts are underway to improve the energy efficiency of PoW blockchains, including optimizing mining hardware and promoting renewable energy sources.